Cash Talks

The Impact of Financial Reserves on NYC Theater Companies

Most Nonprofits Have Less Than Three Months of Reserves On Hand

Source: Nonprofit Finance Fund, State of the Sector 2022 Survey Results

Source: Nonprofit Finance Fund, State of the Sector 2022 Survey Results

Source: Nonprofit Finance Fund, State of the Sector 2022 Survey Results

What is an operating reserve?

Board members of nonprofit organizations will often set aside an Operating Reserve or "Rainy Day Fund" to fund operations in the case of uneven cash flows.

Source: Nonprofit Finance Fund, State of the Sector 2022 Survey Results

This is a Balance Sheet from Second Stage Theater, an off-broadway theater in NYC.

Unrestricted cash and cash equivalents is found underneath current assets.

Source: NYS Charities Bureau

Here, we can see that Second Stage has $4, 981,018 in unrestricted board designated reserves, otherwise known as a cash reserve.

How has the pandemic affected Cash balances at nyc nonprofit theaters?

Performing arts organizations, no doubt, experienced intense economic uncertainty and weathered extremely difficult operational environments during the height of COVID-19. Though PPP (Paycheck Protection Program) loans, SVOG (Shuttered Venues Operating Grants) grants, and ERTC (Earned Revenue Tax Credit) funds helped keep the lights on, how were organizations managing their surpluses and deficits?

Let's take a look at a sample set of NYC Nonprofit Theaters to measure how the pandemic has affected their cash balances.

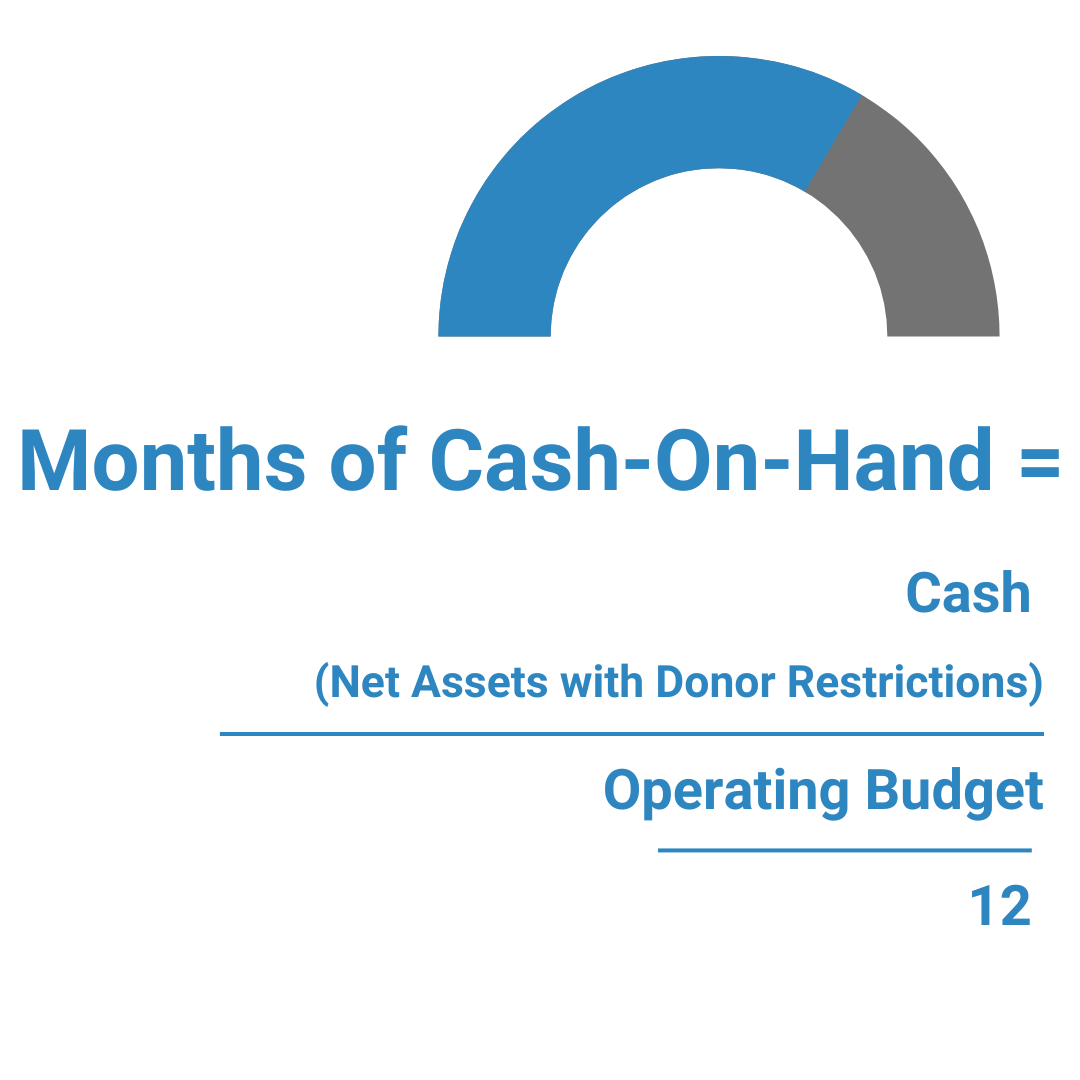

What is Cash-On-Hand?

A nonprofit organization's cash-on-hand is the sum of all unrestricted cash and cash equivalents. Unrestricted cash and cash equivalents are cash that are not restricted by purpose or time. Months of cash-on-hand is a useful metric to democratize how we measure unrestricted cash across organizations that are very different in size.

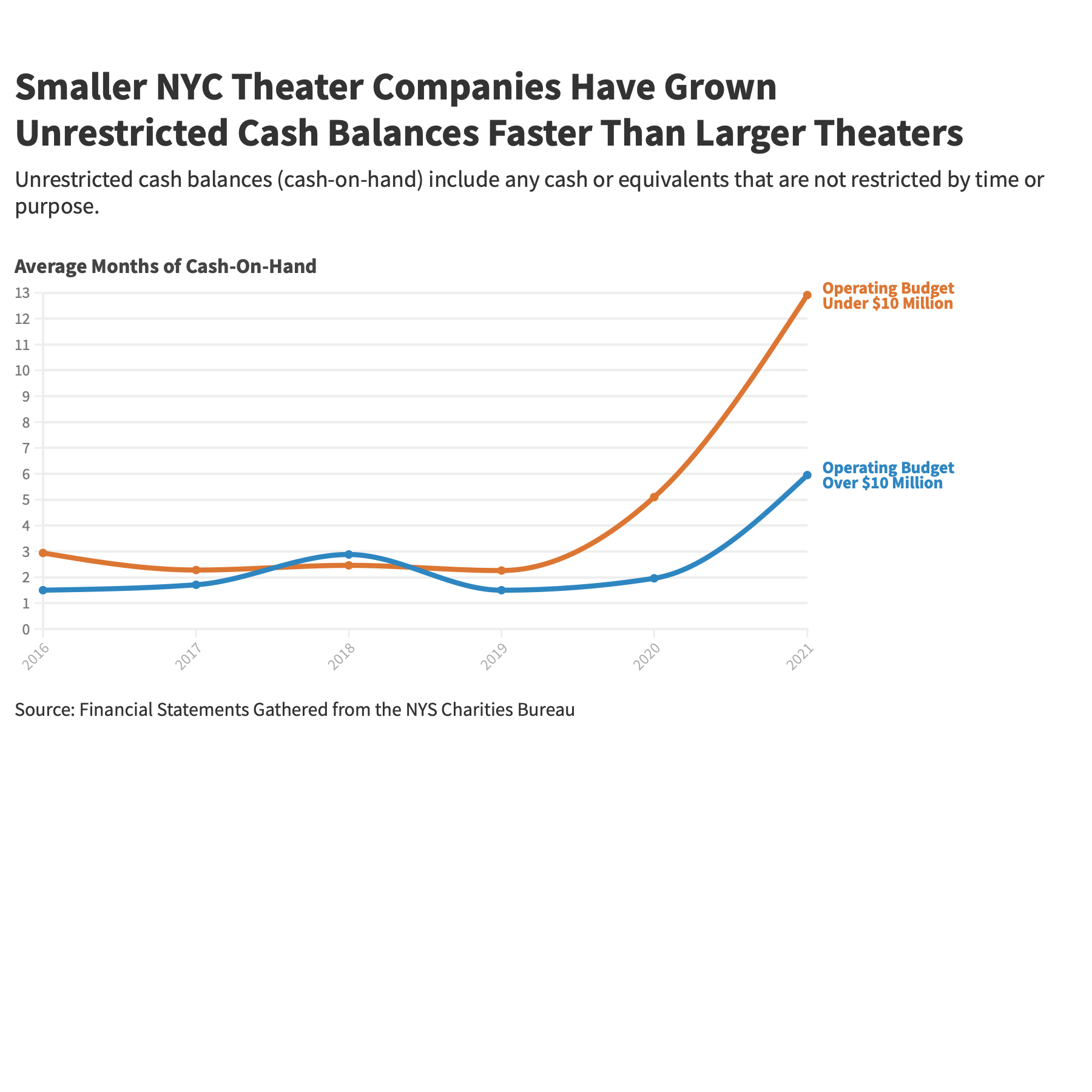

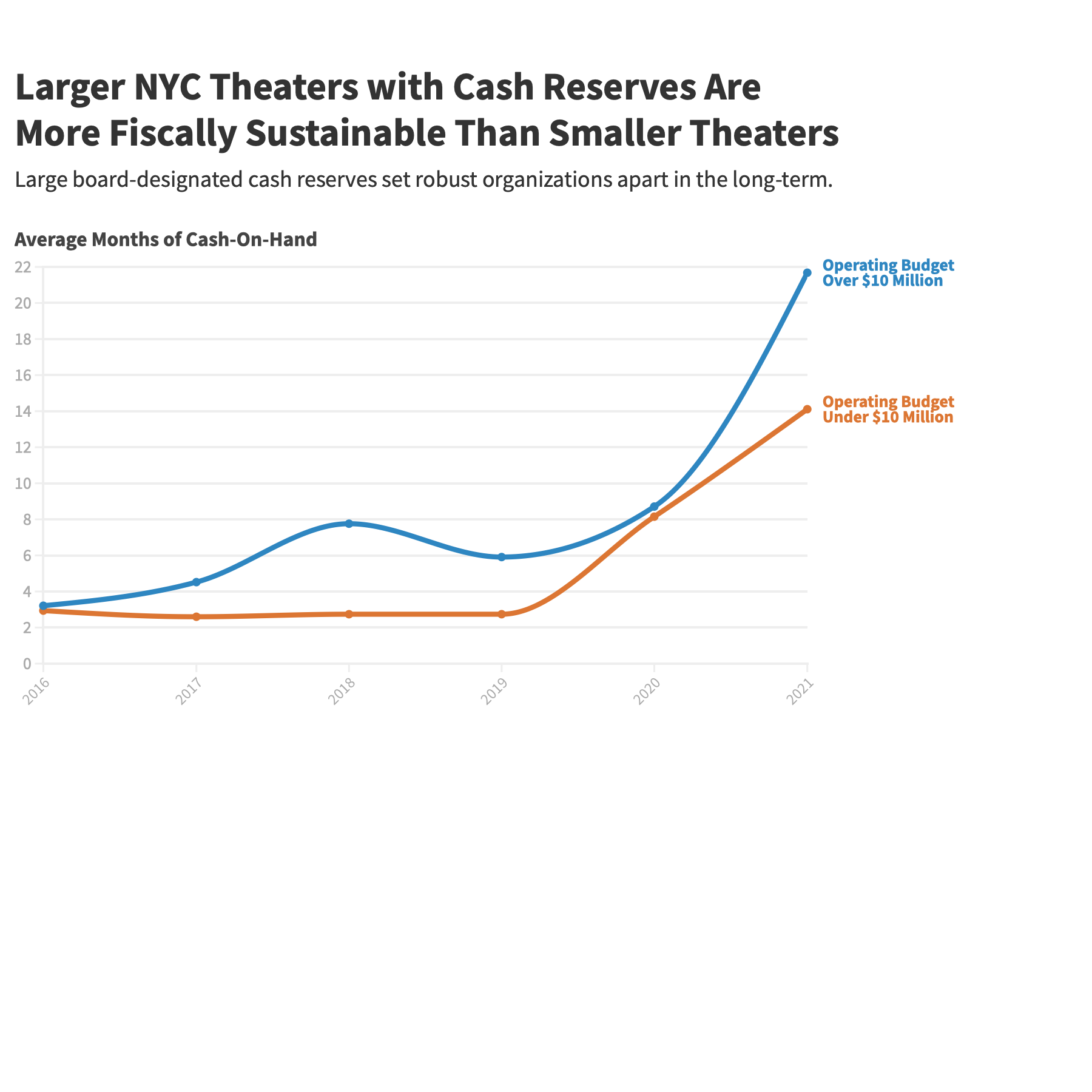

On average, smaller NYC Theater companies have grown unrestricted cash balances faster than larger theaters.

Between 2016 and 2019, months of cash-on-hand stayed relatively low for smaller organizations with operating budgets under $10 million. For example, Second Stage Theater had 1.34 months of cash-on-hand at the end of FY17, but in FY18 they had 4.76 months of cash-on-hand.

Beginning in 2020, months of cash-on-hand began to rise for both large and small theaters. In 2021, the average small NYC theater had almost 13 months of expenses in cash available. Surprisingly, larger theaters experienced didn't increase their unrestricted cash balances as fast as smaller organizations by 2021.

These large increases in unrestricted cash in 2020 and 2021 are largely attributed to the effects of the COVID-19 pandemic and cancellation of all live performing arts events. Even though ticket sales were essentially non-existent, NYC theaters were still spending a fraction of what they had normally spent on a typical season pre-pandemic.

But that doesn't tell the full story.

Operating reserves set more robust organizations apart in the long-term.

Organizations with unrestricted operating reserves have larger cash levels of organizations without reserves.

When operating reserves are included in the sum of available cash, larger theaters have demonstrated stronger fiscal strength over the past six years than smaller theaters.

Many NYC theaters with substantial reserves emerged from the COVID-19 shutdown with higher levels of unrestricted cash than pre-pandemic.

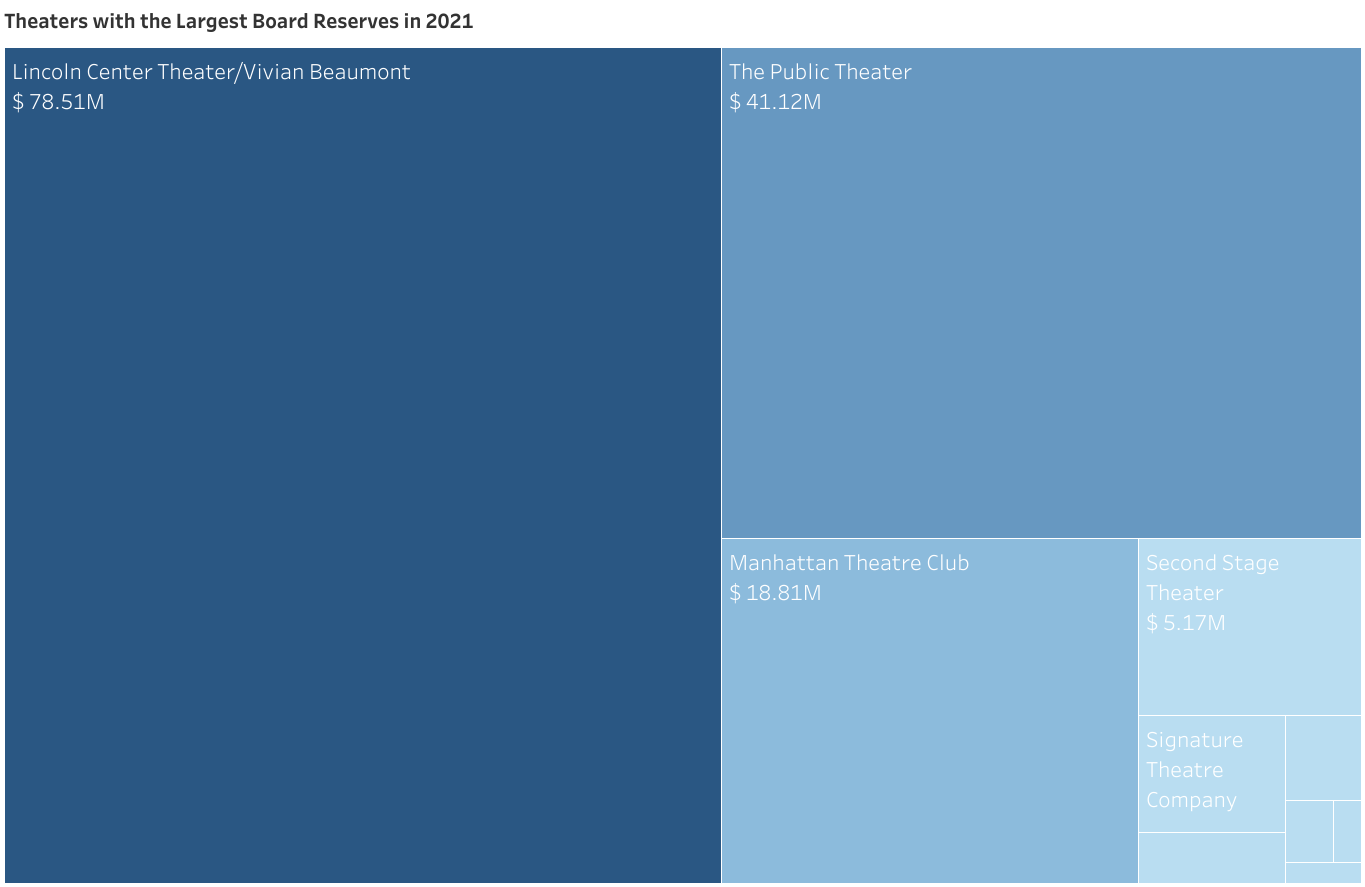

Lincoln Center Theater and Manhattan Theatre Club are two examples of organizations with behemoth reserves.

Organizations like Lincoln Center Theater, The Public Theater, and Manhattan Theatre Club have some of the largest reserves in the theater industry.

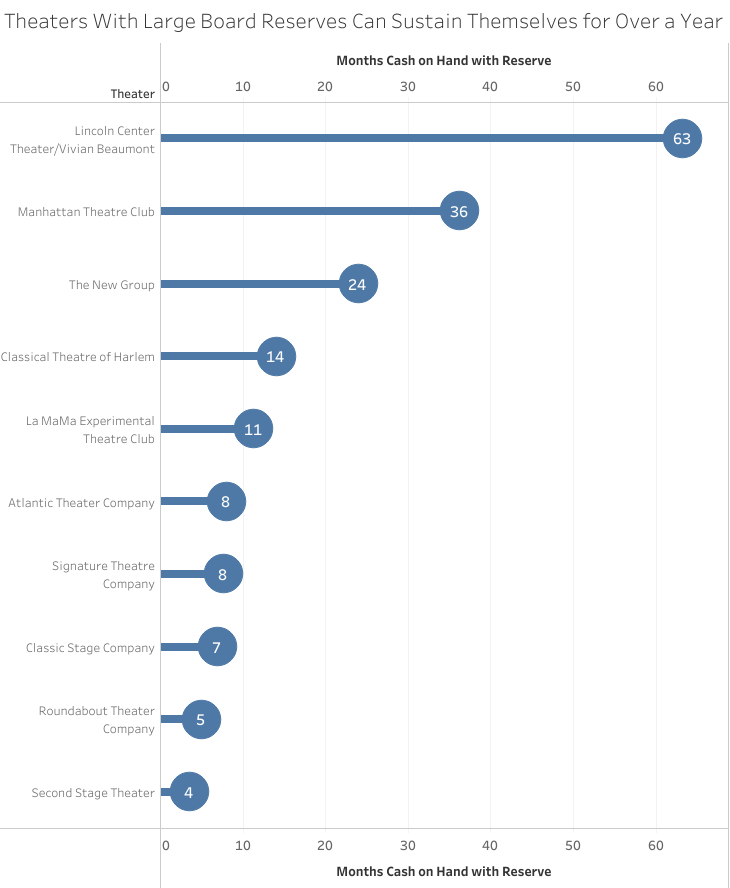

Combining their board reserve and cash, Lincoln Center Theater could pay it's monthly expenses for 63 months. That's over five years!

But even for more nimble organizations with smaller budget sizes, having a designated operating reserve set aside is a wise financial strategy. At the end of the day, a reserve is the organization's "savings account" and is adaptable to their financial needs and flows.

Most nonprofits have experienced a drastic impact on their programs and financing throughout the COVID-19 pandemic. But research shows that nonprofits with reserves were less likely to reduce operating hours, lose staff, or experience difficulty paying employees or vendors for their services.

Source: Kim, Mirae, et al, "Are You Ready: Financial Management, Operating Reserves, and the Immediate Impact of COVID-19 on Nonprofits," December 2020.

Establishing an operating reserve is wise for any theater to prepare for future fiscal uncertainty.

Steps to Establish an Operating Reserve in Your Nonprofit

Speak with your Board of Directors and Finance Director

The Board of Directors will need to approve the implementation of an Operating Reserve fund in your organization.

Photo by Will H McMahan on Unsplash

Photo by Will H McMahan on Unsplash

Establish a cash reserves policy

The board of directors may adopt a “reserve policy," as they are the governing body with fiduciary oversight. Consider including guidance on how much the nonprofit will set aside, defining the circumstances that removing reserve funds will be enforced under, the process the nonprofit will go through to determine whether or not to dip into reserves, and how the nonprofit will repay into the reserve account.

Photo by Andre Taissin on Unsplash

Photo by Andre Taissin on Unsplash

Start saving!

Communicate with your Bookkeeper and Banker to start the reserves process.